Based on credit scores, Americans appear to be doing well financially. Average FICO credit scores have risen steadily over the past decade, from 690 in 2012 to 716 in 2022.

Credit scores are often used as a proxy for financial health; however, consumer financial behavior in 2022 did not promote financial fitness. High inflation and interest rate increases throughout the year stress-tested consumer finances. Despite solid credit scores, consumer financial fitness is under pressure.

Behaviors Indicating Poor Financial Fitness

There are certain behaviors that indicate poo financial fitness. They include borrowing just to make it through the day-to-day, relying on credit cards, and spending more money despite inflation, among others. These behaviors were observed in 2022, indicating poor financial health, despite the continual increase in credit scores.

Borrowing to Make Ends Meet

Interest rates rose sharply in 2022, yet American consumers pushed borrowing to a new level. Federal Reserve data shows that consumer debt was at an all-time high at the start of 2022 and continued to rise throughout the year, even though interest rates jumped from near zero to above 4% in 2022.

This surge in borrowing despite rising interest rates is a symptom of the strain of high inflation on household budgets. People with incomes no longer sufficient to make ends meet borrowed to bridge the gap. An understandable reaction, perhaps, but not a financially fit and sustainable approach for the future.

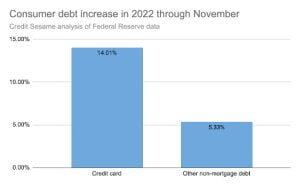

Relying On Credit Card Borrowing

Over the first 11 months of 2022, consumer credit card debt grew by 14.01% compared to 5.33% for other non-mortgage debt.

Credit card interest rates are generally much higher than loan interest rates. If borrowing is necessary, taking out a personal loan makes more sense. But it takes financial knowledge and planning to understand that lower-interest, longer-term installment borrowing may be a better solution. When consumers go to the store and find prices higher than expected, reaching for their credit card is a natural response. However, it is not the best response for financial health.

Spending More Despite Inflation

Inflation stress may take the blame for some of the increased consumer spending, but there is more to it. According to the Bureau of Economic Analysis (BEA), consumer spending rose by 2.2% in 2022 after adjusting for inflation.

In other words, while rising prices stretched budgets, consumers chose to buy even more, funded by credit card debt.

It is possible that people were making up for lost time after pandemic restrictions and using money they had not spent during shutdowns. This is not a financially savvy move in a year of high inflation, high interest, and the threat of recession looming.

Reducing Personal Savings Rates

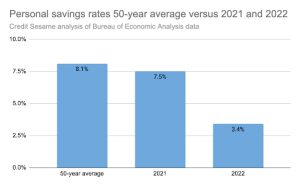

Savings rates dropped as spending increased during 2022. Bureau of Economic Analysis data gathered over the past 50 years shows the annual personal savings rate has averaged 8.1%. This is the percentage of income that consumers have left over after taxes, expenses, and spending. In 2021, the savings rate was a little below the 50-year average. In 2022, the savings rate dropped by more than half, but overall consumer savings stayed at a healthy rate suggesting that consumers may soft-land any mild recessions.

Consumer spending exceeded the inflation rate using funds financed by expensive credit card debt and at the expense of saving – not a financially astute move.

The Failure of Credit Scores As a Measure of Financial Fitness

Credit score indicates if a consumer is a reliable borrower based on past and present use of credit. It is possible to have an excellent credit score right up to the moment of financial meltdown from job layoff, mounting debt, growing credit card balances, depleted savings, and no liquid funds for any new or extra debt or emergencies. Credit Score is not a financial fitness indicator.

The good news is that rising credit scores mean Americans are in a better position to borrow money. However, a consumer’s financial fitness depends on many more factors than their credit score, and irresponsible borrowing can lead to a deterioration in financial health.

Trying to assess financial health based on credit scores alone is like judging academic prowess after reading a report card on one academic subject. A high score in one subject does not mean an individual is guaranteed broader academic success.

Good credit scores give consumers access to low-cost capital, money-saving possibilities, and opportunities to own a home and build wealth. However, credit scores fall short in assessing other aspects important to one’s financial fitness, such as:

- Income

- Cashflow

- Savings

- Overall financial management

Does the consumer have adequate income and cash flow to pay their obligations comfortably? Are they saving money for the future? Can they afford to take on new debt? Do they have enough savings and assets to weather a financial storm like losing a job? Are there funds available for an emergency? Are they managing their current financial circumstances well or barely making ends meet?

It can be argued that one sign of financial fitness is relying less and less on borrowing to maintain a lifestyle into the future. A recent Credit Sesame survey found that 43% of people with good credit scores (670 to 739) do not have sufficient saved funds to survive more than three months if they lose their job or other sources of income. This illustrates clearly that a good credit score is a starting point but in itself does not necessarily lead to financial fitness and security.

America needs far more than a credit score to assess consumers’ true financial fitness in uncertain times.

Credit Sesame Survey Methodology

The Credit Sesame Credit and Financial Fitness Survey December 2022 were designed and executed by Credit Sesame using the WebEngage survey tool. The survey sample comprised over 1,500 Credit Sesame members with a credit score distribution resembling the U.S. general population. In aggregate, the sample data is accurate, with a 2.5% margin of error using a 95% confidence level.