Governance tokens in decentralized finance, or DeFi, have suddenly jumped into prominence

The U.S. government’s response to current economic conditions has put significant pressure on fixed income instruments. Low Interest rates contribute to a decrease in yields and the Fed is not in a hurry to raise them.

While traditional fixed income vehicles do not appear attractive any longer, the soaring DeFi space offers blockchain-based alternatives. Still, these tools are rather sophisticated and need to be treated with caution.

The problem with fixed income

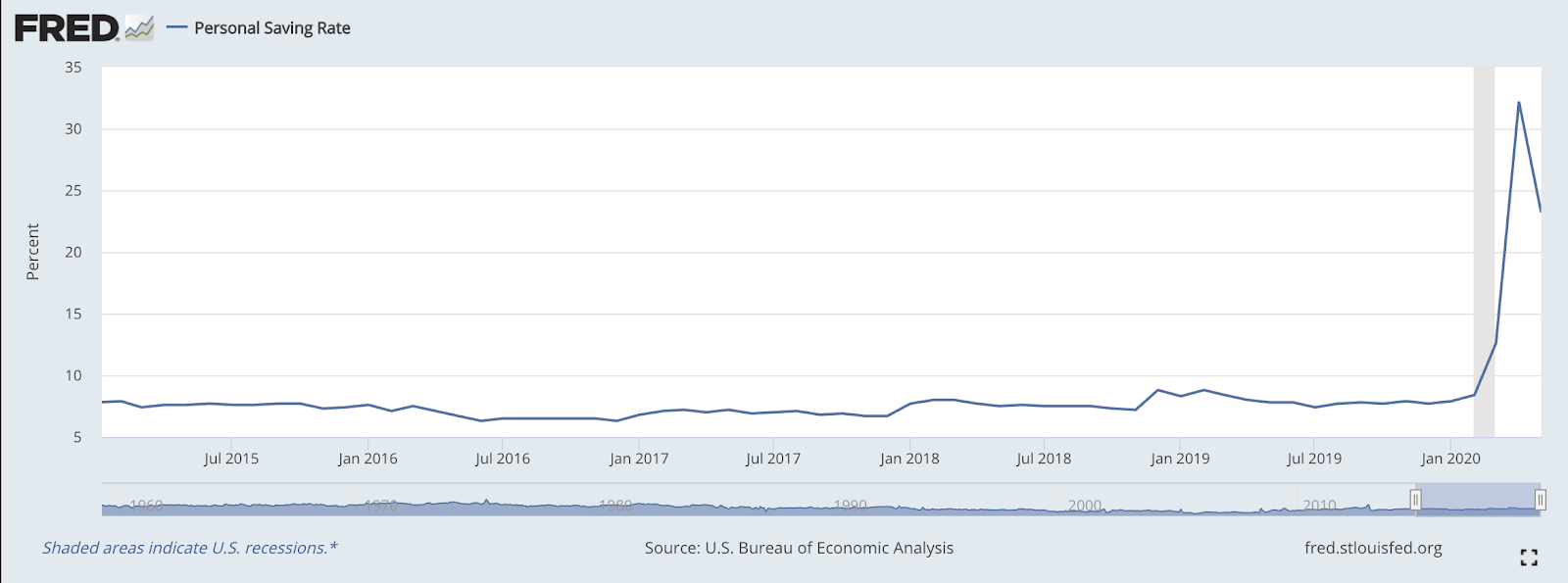

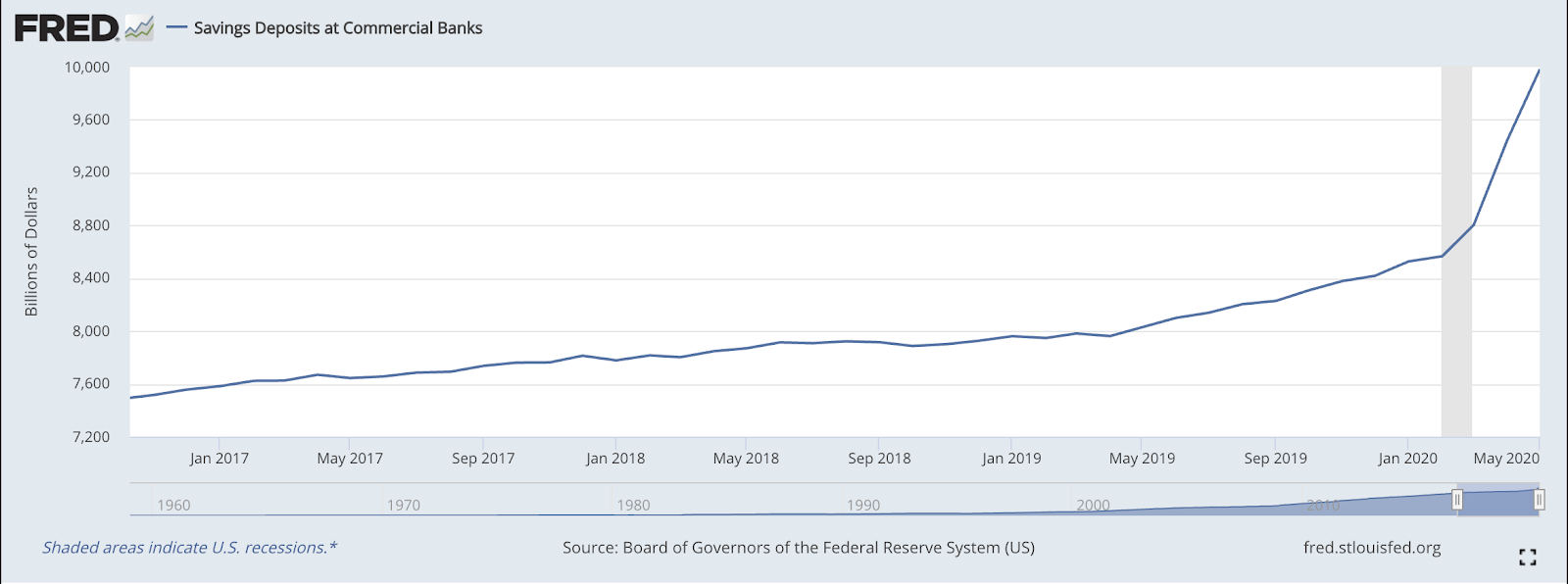

Although the stock market has quickly rebounded from its devastating March lows, the U.S. economy doesn’t appear to be completely out of the woods. It makes sense that in such circumstances people favor saving up liquid cash for possible emergencies.

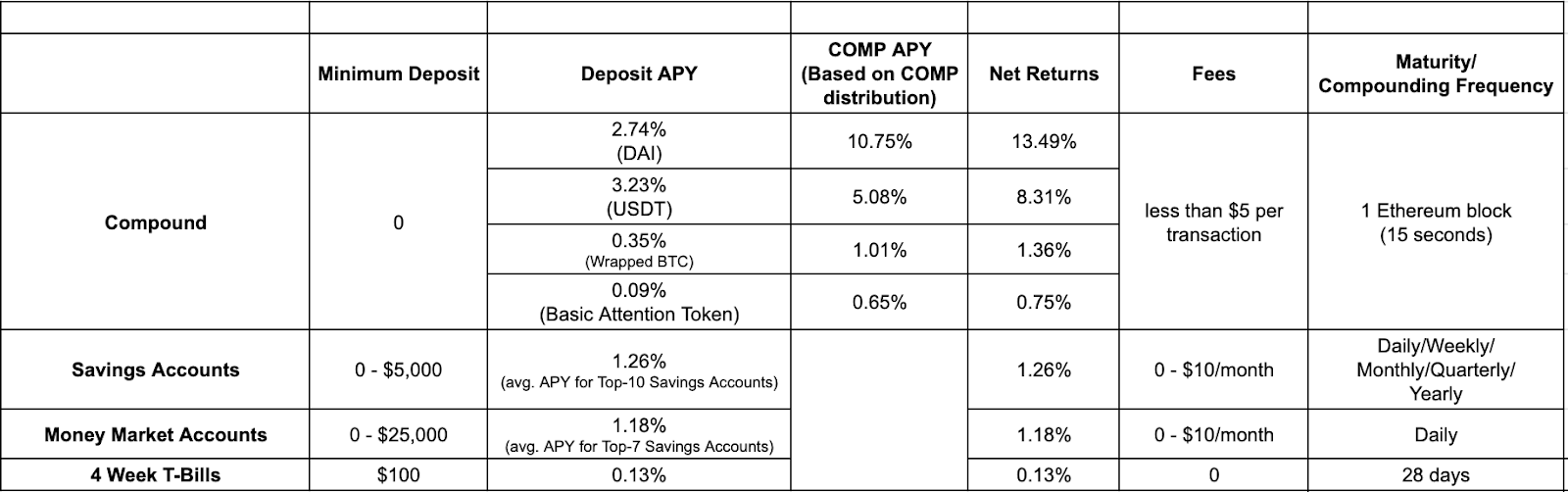

The personal savings rate and savings deposits in commercial banks are shooting through the roof. However, the yields have shrunk substantially. The top-10 online banks’ savings accounts provide an average annual percentage yield (APY) of 1.26%, a far cry from the rates observed in 2019.

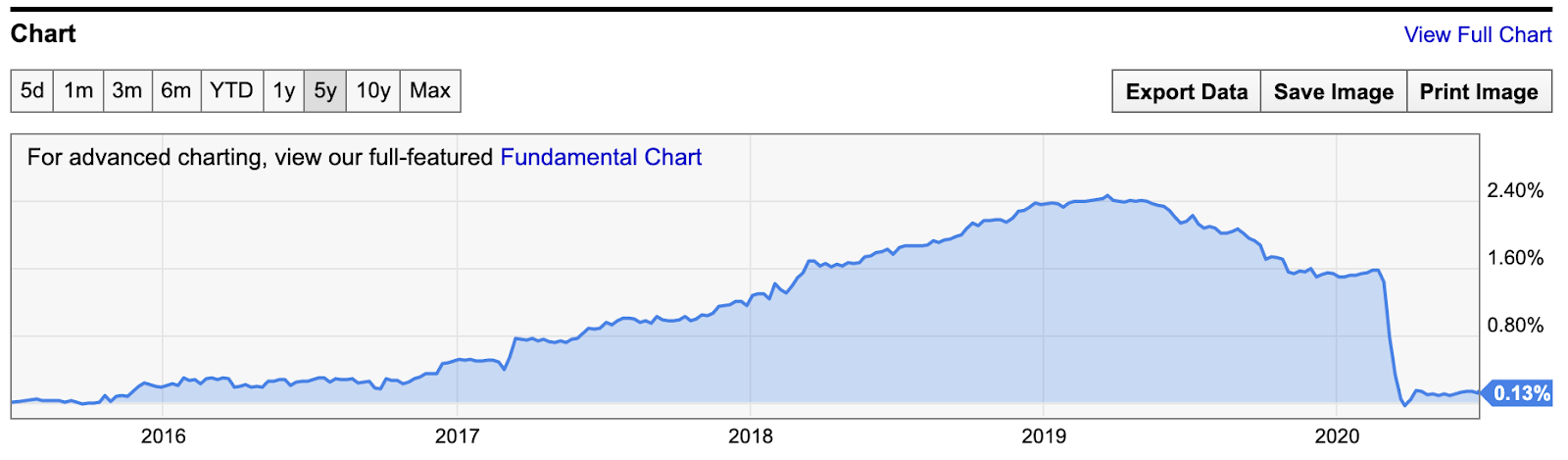

4-week T-Bills’ yield took a strong hit as well. The discount went from 1.57% in February to 0.13%, over a 90% decrease.

The beauty of fixed income instruments is that they enable people to keep their savings liquid, as opposed to less liquid stocks and bonds while still earning interest. However, the Fed’s monetary measures put constraints on what traditional instruments can offer.

What if there was no pressure on the interest rates?

Enter DeFi

Decentralized Finance, or DeFi, is an ecosystem of financial instruments running on top of various blockchain platforms. Smart contracts have provided the necessary infrastructure for fully automated alternatives to traditional lending and trading platforms.

At the beginning stages, DeFi platforms are usually stewarded by their creators. However, later, governance is passed to the community and maintained through voting among token holders. Hence, changing how interest rates are calculated depends on the community and algorithms, not a centralized party.

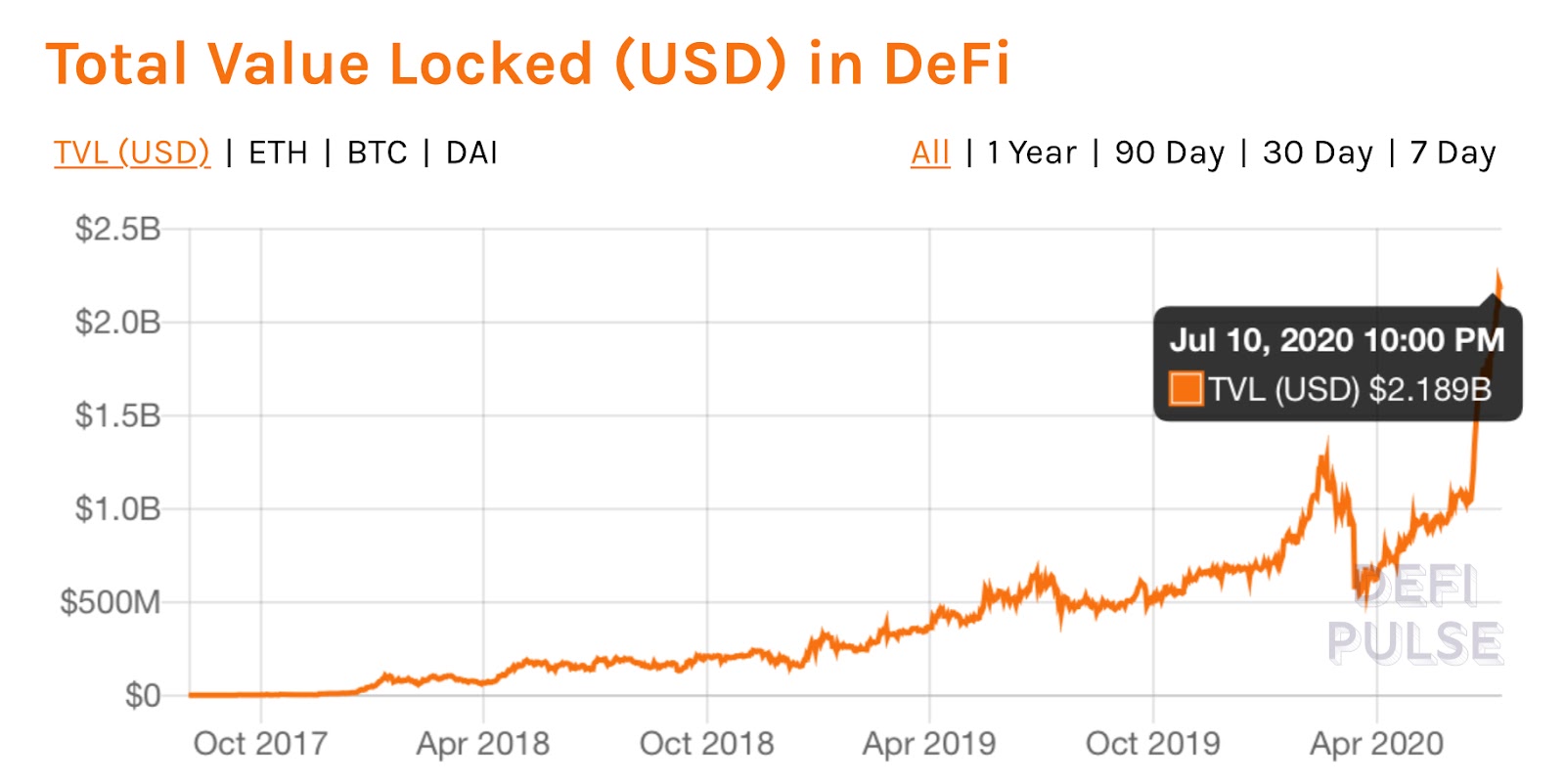

DeFi sector started to pick up from the latter half of 2019 and except for a short-term decline in Spring 2020 is full steam-on. To date, the total value locked in DeFi exceeds $2 billion. The major driving forces of this surge are attractive interest rates and yield farming.

“DeFi is an evolution of a parallel economy where novel incentive mechanisms dictate everything”, says Rosh Singh, CEO at Quadency—a professional cryptocurrency trading platform.

Not-So-Passive Income

DeFi instruments have much less friction than their traditional counterparts. Hence, moving funds back and forth various platforms can multiply the baseline interest rates. As a result, with compounding and bonuses, annualized yields may exceed 100%, a stellar difference with keeping money in a bank.

At the moment, DeFi development is largely concentrated on Ethereum. The most popular platforms include Maker, Compound, Synthetix, Kyber Network, and Uniswap. The combination of all of the platforms creates a mesh of different services enabling swapping tokens and borrowing/lending them in a matter of minutes.

The gold-rush of DeFi is referred to as ‘yield farming’. Farmers utilize exotic strategies such as multi-step transactions and flash loans to take short-term advantage of how algorithms work. A flash loan is a loan taken and repaid almost instantly, which sometimes enables borrowers to get loans without providing collateral because of the speed at which smart-contracts function..

As DeFi’s popularity grows, the interfaces of the tools used for farming will become more user-friendly for average users, driving even more people into the ecosystem. For instance, with Furucombo it takes only a few clicks to generate a transaction that shoots instantly across multiple platforms. A user specifies how they want to execute a transaction in a convenient UI, and the platform generates a multi-step transaction that previously required significant programming skills.

Increasing ease of access, flexibility, and hefty yields keep driving more people to tap into DeFi space. What do newcomers see?

Compounding With COMP

Compound is a great example of an algorithmic platform focused on lending and borrowing crypto assets. Its major advantage compared to the traditional instruments is that its interest rates are a function of the supply and demand, they are not bound by any external forces.

From a lender’s perspective, Compound works like a Certificate of Deposit (CD), except that a contract’s maturity is only about 15 seconds. Compound looks similar to very short-term vehicles such as Money Market Accounts and 4-week T-Bills.

Currently, the yields on assets on Compound are significantly more attractive than what is offered in the traditional space. There here is far less friction to start lending the minimum deposit amount and undergo KYC.

Compound’s decentralized nature and reliance on algorithms creates potential threats for the platform’s users. Interest rates are attractive but carry smart contract risks that vary based on market conditions.

Higher reward = higher risk, BAT example

Basic Attention Token (BAT) recently had the highest APY on Compound, roughly 13%, 10 times the average APY of top-10 savings accounts. There are a few caveats that result from such an outperformance.

For starters,, BAT is less liquid than cash and it has substantial volatility. Hence, it’s not very suitable for savings purposes. Moreover, given the maximum draw down of more than 60% each year, lending BAT for a longer time frame is not reasonable.

Second, there has to be sustainable demand for BAT to keep the equilibrium in interest rates high. Speculative activity does not support the yields for long.

Third, BAT was used as a proxy for earning COMP. COMP is Compound’s protocol token that represents ownership and enables governance participation. It has recently soared to over $200, making it a lucrative target for speculators.

The key to earning the highest possible amount of COMP is to participate in a pool with the highest liquidity. Hence, speculators were playing with the BAT market as long as they could make money off COMP. However, after the change in COMP distribution rules the speculators left and the interest rate plummeted.

Besides systematic risks, DeFi instruments carry technological ones. Smart-contracts are complicated and the classic approach of building fast and breaking things doesn’t apply because of the amounts of value they process. Smart-contracts need to undergo both internal and external audits before going into production. Investors should verify that companies have publicly published proof of a professional third-party audit of all smart contracts and protocols.

“For institutions to have meaningful participation in the decentralized financial infrastructure using a centralized overlay service may be unavoidable. Assuming the US and EU financial ground rules remain unchanged, issues such as regulatory compliance and volatility protection are likely to require some level of a centralized layer to satisfy institutional concerns.” says Nuke Goldstein, CTO of Celsius—a crypto lending company.

Every tool has its use

DeFi is young and complex. Through platforms like Compound, users have opportunities to earn interest on savings even in the context of low-interest rates.

Making use of DeFi tools requires understanding how they work, lest interacting with them may lead to losses. Overleveraging and volatility creates moving parts that increase risk in an environment solely controlled by algorithms. Hence, any instruments with high yields should be scrutinized before making any investment decisions.